Miner Extractable Value (MEV) burst onto the scene in the summer of 2020 with the appearance of Ethereum’s on-chain marketplace of DeFi apps, such as Curve, Uniswap and Compound.

At first, only the technically inclined could profit off the practice of sequencing trades for extra profits. That is until Flashbots introduced a new Geth software specifically for mining pool and trader interactions earlier this year. Since then, over 85% of Ethereum mining pools have implemented sequencing software.

Want more mining insights like this?

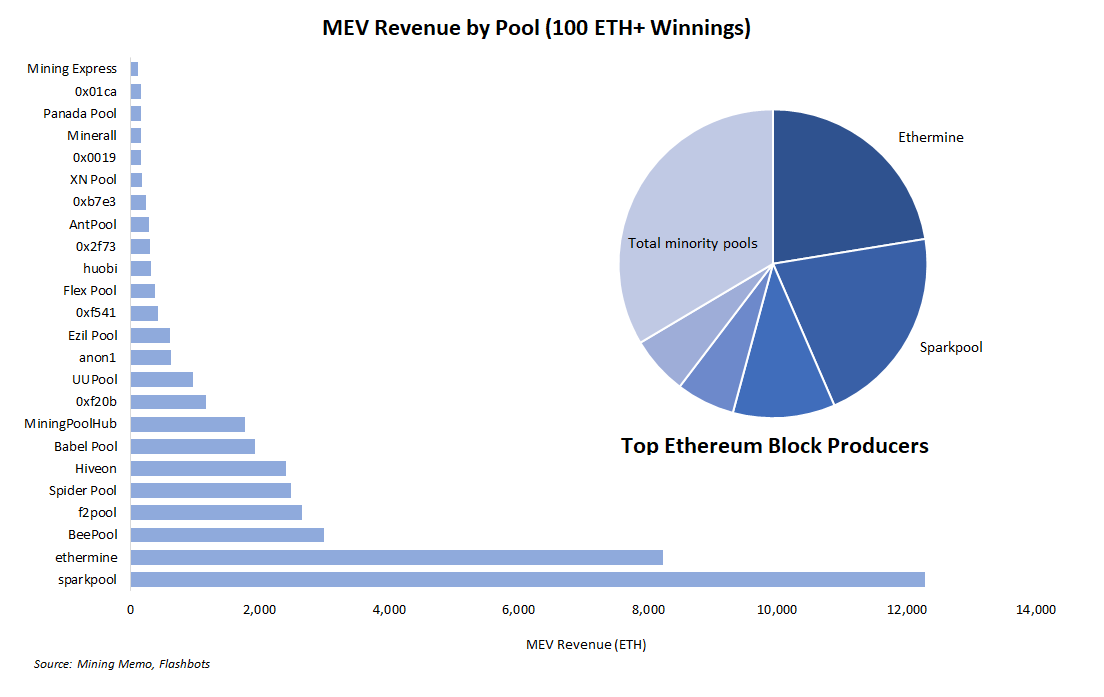

Data from May to July shows how much Flashbots succeeded by turning the MEV marketplace into just another hashrate-based calculation. Hashrate and extraction are highly correlated, meaning it makes sense to see larger players dominate the MEV game compared to the little guys.

In other words, extraction and hashrate should be proportional.

It’s an impressive sign given that only one or two Ethereum pools operated MEV desks as of February 2021.

- At that time, it was anyone’s guess how miners would take advantage of their privileged sequencing position or how traders would leverage their alpha.

- In fact, some referred to Flashbot’s miner marketplace as encouragement of outright theft.

But the standardization of MEV via Flashbots now makes it clear hashrate and value extraction should play an intimate role going forward. In order to keep one’s share of MEV revenue, one must continue adding hashrate comparatively to other pools.

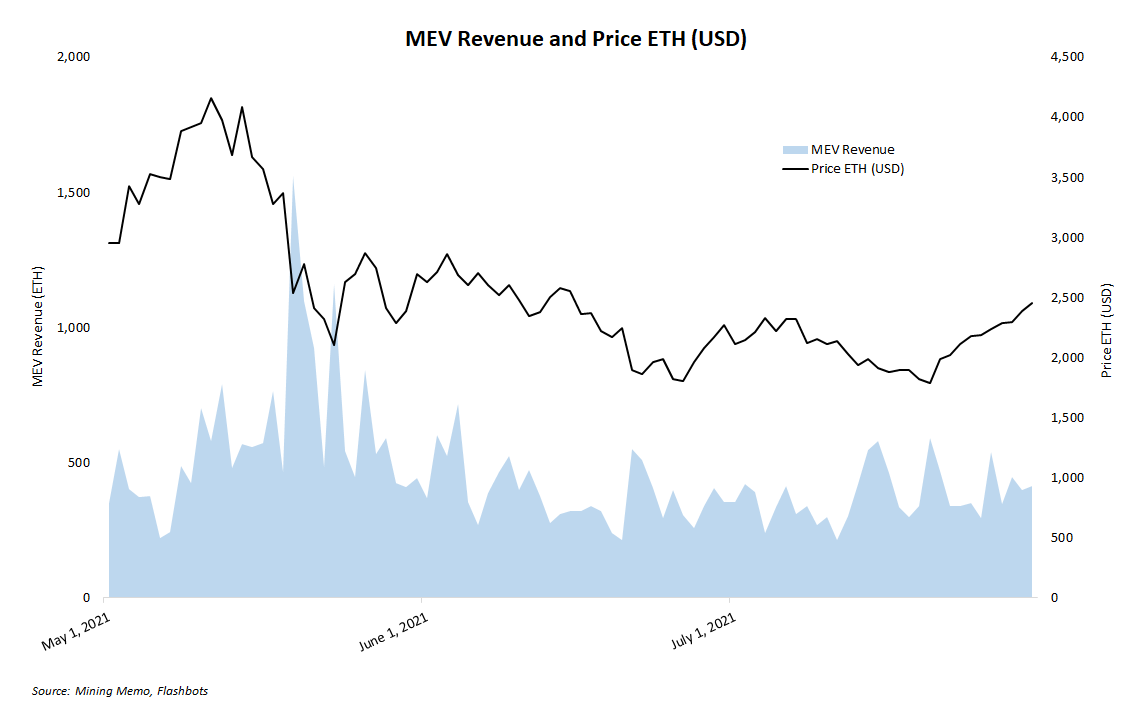

Similar to standard transaction fees, MEV profits follow the ebbs and flows of ETH’s price, itself a partial reflection of on-chain activity. When ether’s value falls, so does on-chain activity leading to lower MEV and vice-versa.

As of now there is little indication that Ethereum miners are price sensitive to MEV fees charged by pool, particularly as MEV revenue by mining pool has dropped significantly over the summer months.

For example, SparkPool’s MEV returns are as little as 1% of total block rewards as of writing. Mining pools typically collect fees for sequencing transactions from traders and retain upwards of 10%. And although seemingly inconsequential, small MEV fees are one of the few spaces of competition between Ethereum pools.

Thanks to Robert Miller for Flashbots data.